Think of the word “credit” as something similar to “credibility” — the two words do share most of the same letters, after all. Whether personal, business, or otherwise, your credit and subsequent credit score determine your financial viability and risk factor for companies to lend you something. Typically, what’s being lended comes in the form of invoice factoring, asset-based loans, or a small business line of credit.

Small Business Creditworthiness From Our Perspective

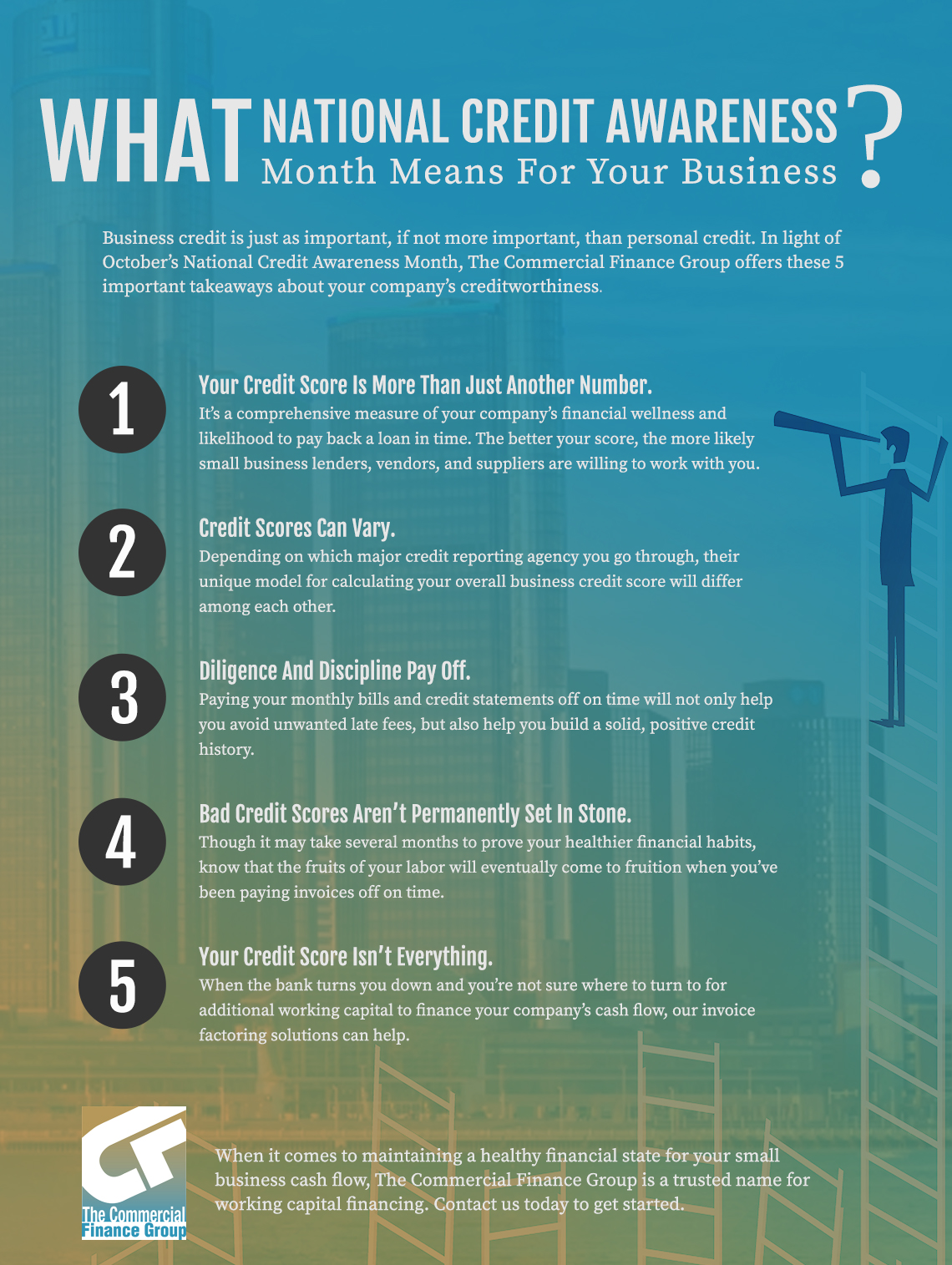

At the end of the day, when it comes to qualifying for just about anything money-related, it’s all a matter of credit. We’re in the business of lending additional capital to SMB organizations here at The Commercial Finance Group, and because it’s the month of October, we only saw it fit to raise more awareness about the importance of credit. That’s right: October is National Credit Awareness Month, and though that statement alone won’t spark much excitement for most people, it definitely captures our interest!

Our Small Business Lending Solutions

When your company’s cash flow is tied up in pending payments from vendors, customers, and suppliers, don’t wait idly to receive these payments and ignore the pressing need for growth in your business. Through invoice factoring and asset-based loans, The Commercial Finance Group can help alleviate common cash flow problems with the help of working capital. Providing you with the liquid capital you need to run day-to-day operations, we’re proud to get you the financial solutions you need in a fraction of the time it takes banks to process loans.

In this blog post, we’re going to delve a little bit deeper into National Credit Awareness Month and what that means for small business owners like you. Let’s get started.

The Importance Of Keeping Business and Personal Credit Separate

This financial awareness month is largely intended for personal credit purposes. Of course, this is important information for millions of people who either don’t understand the nuances of credit, what determines creditworthiness, or how credit can affect future purchasing decisions.

So, while credit is very important in the context of personal money management, it’s equally as important for your company. All too often, entrepreneurs tend to get their personal life and business life entangled, which isn’t necessarily a bad thing. However, we’d advise you to keep your personal credit and business credit completely separated. Here’s why:

Business Loans Can Affect Personal Purchases

With your own Social Security Number on the line, getting a loan as a new business owner means that any business credit reports are tied in with your personal credit reports. For established SMB owners, this isn’t necessarily a bad thing. For many entrepreneurs who are just getting their foot in the door of the backbone of America’s economy, however, this could spell bad news.

Indeed, small business loans could eat up or drastically reduce your ability to borrow as an individual. Why? Lenders will take a close look at your debt to income ratio, and when you’re borrowing more than you’re taking home (and what emerging small business doesn’t do this?), you’re painting a bleak personal credit picture to the lenders in question.

Business Loans Offer More Credibility

We’re already back to the term “credibility,” and that’s because it’s integral to creditworthiness. Borrowing in the name of your company is going to lead to better terms, better financing, and even increased sales. When you borrow, you’ll have to pay less in interest if you have a strong business credit score that’s separate from your personal score.

Additionally, suppliers and vendors are more likely to work with you when you have strong numbers to back your creditworthiness. This is leagues better than just hoping that someone out there will work with an entrepreneur who’s tied their personal and business credit too closely.

Credit-Building Basics As a New Small Business Owner

Not unlike building personal credit, you’ll simply want to borrow money and pay it on time, in full, every month. However, it’s not entirely that simple. Here are a few key aspects of building small business creditworthiness from scratch:

- Get an Employer Identification Number (EIN) via the IRS. You’ll want to use this in place of your Social Security Number in all business situations, loan applications, vendor and supplier relations, and when you go to file your company’s taxes.

- Learn more about incorporating your business. Depending on the nature of your business, incorporating may pose significant financial advantages, especially when it comes to rapidly gaining credit. An attorney is the most credible source for legal matters such as this.

- Open a business checking account. In many cases, banks offer free business checking. Open the account in the name of your business with your EIN.

- Work with suppliers and maintain good relations. If you’re paying them within the 30- to 60-day time period, and vice versa, you’re gaining credit. If your vendors and suppliers aren’t paying you in time, that’s where our invoice factoring and asset-based loans come into play!

It’s Never Too Late To Improve Your Credit Situation

Your credit score will always follow your small business around, so it’s always worth checking up on and improving. For financial assistance that goes well beyond a traditional small business line of credit, The Commercial Finance Group can help. In light of National Credit Awareness Month, we wish you a lucrative Q4 this year and a healthy cash flow situation. To learn more about our invoice factoring services, don’t hesitate to reach out to us today.