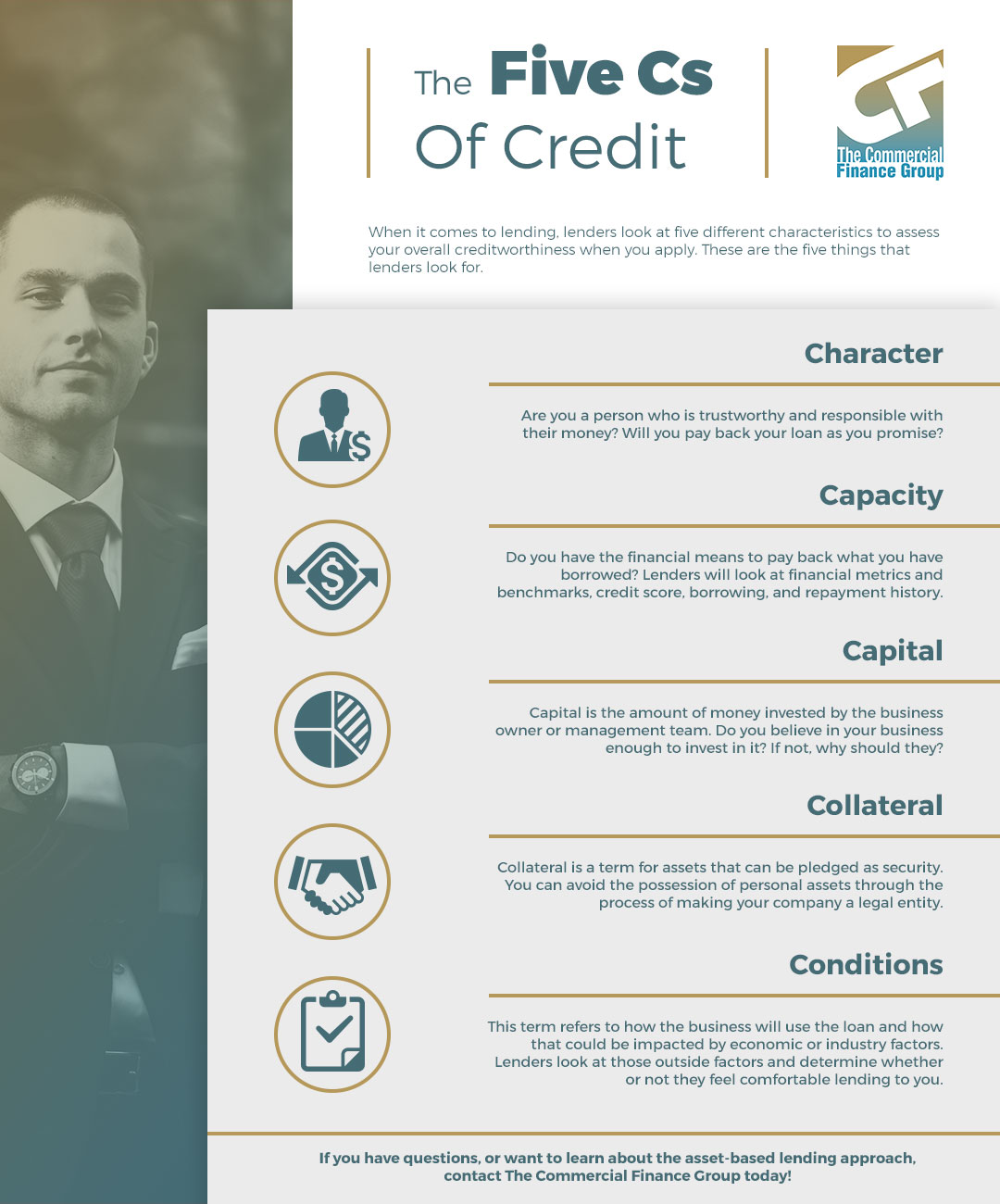

When it comes to lending, each lender takes time to make sure that each applicant is worthy of a loan. Will they be able to pay the loan back? Are they trustworthy? Do they have the credit of a responsible individual? These are all questions that lenders ask when reviewing loan applications.

There is a system lenders use to gauge the creditworthiness and trustworthiness of potential borrowers. The system is called,“The Five Cs Of Credit.” The five Cs stand for: character, capacity, capital, collateral, and conditions. This method incorporates both qualitative and quantitative measures. Lenders will look at a borrower’s credit reports, credit score, income statements and other things relevant to the borrower’s financial situation. But what do each of these terms mean exactly?

Character – The first thing that lenders look for is a trustworthy character. Is this individual a responsible person who will do good things with their loan? Will they be honest and consistent about paying it back? They look at credentials, references, reputation, and interaction with lenders. Character is something that you can control. For your best interests in lending endeavors, form a relationship with your bank. Make yourself someone that your bank wants to lend to.

Capacity – Capacity refers to your ability to repay the loan. When it comes to businesses, your business must be able to pay back the loan through cash flow. When it comes to the forms of capacity that lenders examine, they look at financial metrics and benchmarks, credit score, borrowing, and repayment history. Loans are a form of debt, and they must be repaid in full.

Capital – Capital is the amount of money invested by the business owner or management team. Lenders are more likely to lend to individuals who have invested some of their own money into the venture. Lenders often aren’t willing to take on the financial risk unless they see that your business has investment from you or your management team.

Collateral – Collateral is a term for assets that can be pledged as security. Collateral acts as a support if the borrower has trouble or just plain cannot pay back a loan. From tangible assets such as real estate and equipment, to intangible such as accounts receivable and inventory. The borrower’s home can also be used as collateral. Choosing an efficient business structure can help protect your personal assets from being used as collateral if you end up being sued, or if a lender is trying to collect and you cannot repay. Make your company a legal entity can help you secure your business from the risk of losing personal assets.

Conditions – Conditions is a term that means how the business will use the loan and how that could be impacted by economic or industry factors. They examine the conditions under which you are operating your business, and want to make sure those conditions are favorable. They want to identify risks and protect themselves and their investment. They will review the competitive landscape, supplier and customer relationships, and macroeconomic and industry-specific issues and conditions to make sure that risks are identified and minimized.

When you’re looking to pursue a loan, it’s important to examine the five Cs before you apply. If you’ve tried everything and traditional lending is not an option for your company, contact us at The Commercial Finance Group today about asset-based lending options and find out if it’s the answer you are waiting for.